VC Activity

AI and machine learning (ML) startups raised a record-breaking $73.6 billion across 1,603 deals in Q1 2025, marking the highest quarterly total on record by deal value.

- AI captured one in every four VC dollars globally in 2024, a trend likely to accelerate as adoption deepens and infrastructure scales. Capital continues to flow into both horizontal platforms such as OpenAI and Anthropic and sector-specific vertical applications built on top of them. Falling development costs at the application layer are fuelling record deal volume even as funding remains concentrated at the top.

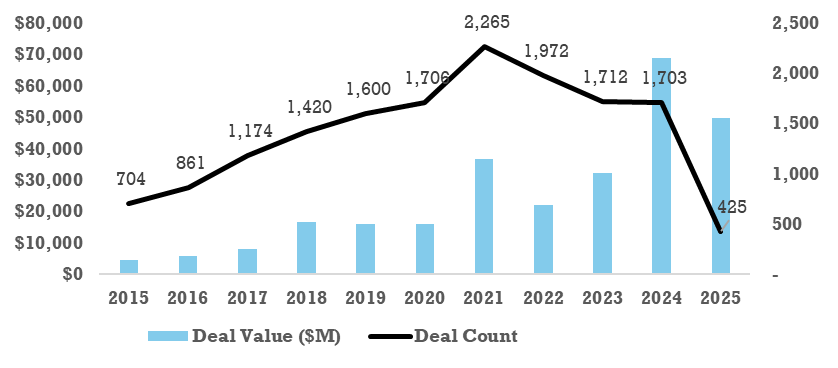

- Platforms like OpenAI and Anthropic captured the big chunk, securing just under $50 billion across 425 deals, accounting for nearly 70% of total capital raised during the quarter. These platforms are general-purpose tools, such as large language models and infrastructures that support a wide range of industries.

Horizontal Platform VC Deal Activity

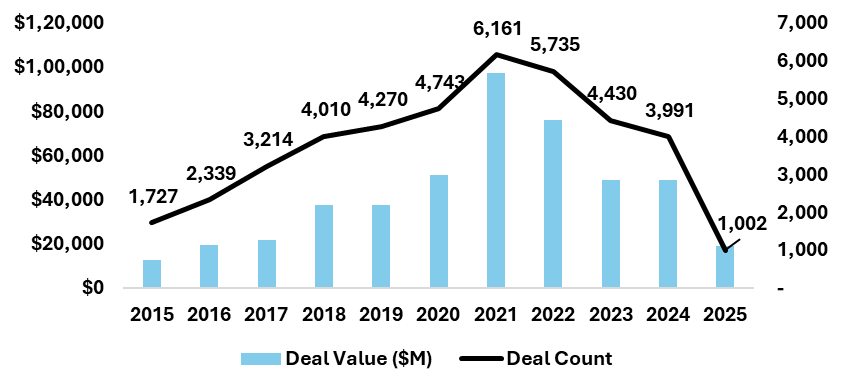

- Platforms in Vertical application startups led in deal volume, notching 1,022 transactions, ~60% of all deals, with an aggregate deal value of $19.2 billion.

Vertical AI applications are niche tools that sit “on top” of those horizontal models, tailored to solve problems in a single sector.

- Vertical models can be developed with just $3 million to $10 million in funding, while horizontal large language model (LLM) development can cost hundreds of millions of dollars at the high end. Lower costs of building applications have reduced entry barriers for startups, enabling them to leverage existing horizontal platforms. The growing deal activity in vertical AI is also fuelled by enterprise demand for tailored, commercially viable solutions across industries.

Vertical Application VC Deal Activity

- Across a trailing 12-month period, Horizontal platforms attracted $107.3 billion in deal value across 1,673 transactions, nearly double the approximately $58 billion raised by vertical applications. However, verticals recorded 3,961 deals over the same period, more than twice the deal volume of horizontal platforms, underscoring a persistent split between capital intensity and deal activity.

VC – Across the Stages

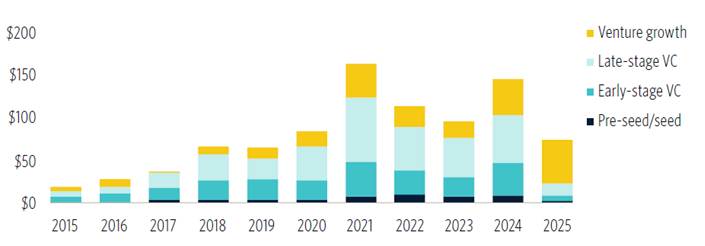

- Venture-growth financing accounted for the bulk of funding in Q1 2025, reaching $49.4 billion.

- Late-stage rounds contributed $14.1 billion.

- While early-stage startups secured $7.3 billion.

The funding pattern remained similar across sub-verticals such as semiconductors, autonomous systems, and industry-specific AI applications.

AI & ML VC deal value ($B) by stage

Source: Pitchbook

Vertical AI Draws more VC Dollars

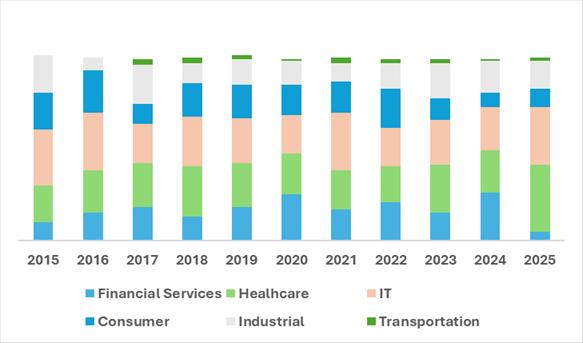

- Within vertical AI, healthcare has proven to be a fertile space for investors. Some $2.1 billion has been invested this year, exceeding last year’s total deal value. From accelerating drug discovery to analysing vast amounts of medical data, healthcare offers significant opportunities for AI-driven improvements.

- Outside healthcare, IT-related vertical AI has been in high demand with investors. Deal value this year has already reached around 85% of last year’s total at $1.8 billion. Many deals in this area involve startups focused on workflow and software automation.

Healthcare claims largest share of vertical AI Funding

VC – Exit Activity

- Q1 2025 recorded 146 VC exits, a marginal decline from 154 in Q4 2024. However, exit value climbed to $27.4 billion, the highest since late 2021.

- Public offerings accounted for most of this at $21.5 billion, compared to $2.7 billion from acquisitions and $3.2 billion from buyouts.

- Deal activity remained skewed toward acquisitions (105), with buyouts (30) and IPOs (11) making up the rest. The strong quarter was shaped by a handful of large IPOs, most notably CoreWeave’s post – money valuation of $14.5 billion and second largest Blocks Group’s with a post – money valuation of $1.9 billion.

Story By Charts

AI & ML VC deal activity

AI & ML VC exit activity

TTM AI & ML VC deal activity by segment

AI fuels uptick in US investor share of European dealmaking

- US investors, who had scaled back activity in Europe during the 2023 downturn, are returning with a strong focus on AI.

- Data shows their participation in 413 AI VC deals worth €7.5 billion (~$8.7 billion), equating to 27% of all transactions and 67% of invested capital in the segment.

Source: Pitchbook

Deal value for European AI startups has seen a significant increase this year as more US investors participate in deals

- U.S participation in European VC activity continues to grow, with 22% of all rounds in 2025 (1,081 deals) featuring American investors—up from 21% last year and matching record levels seen in 2022.

- As Europe’s software engineering workforce has a 30% higher per-capita share of AI specialists than the US and nearly 3x that of China, making it a strong talent hub for Europe’s deep AI talent pool that attract cross-border capital.

- For European startups, US capital provides higher valuations, greater liquidity, and smoother exit pathways, especially critical given Europe’s relative shortage of late-stage financing.

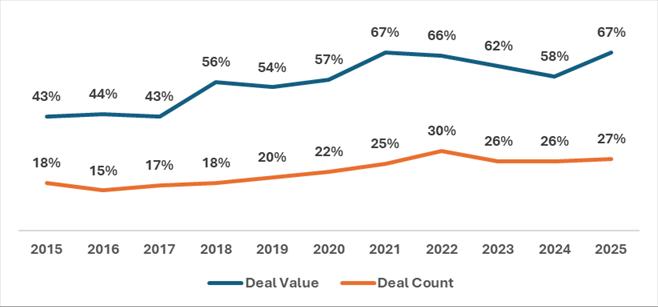

US investors’ share of European AI deal value and count is trending upwards this year

Source: Pitchbook

Key Findings

- US investors’ share of deal value has risen sharply since 2017, peaking above 65% in 2021 and stabilizing in the 60%+ range. This indicates their preference for larger, high-value transactions, often in late-stage or growth rounds.

- While deal value surged quickly, deal count grew more gradually from ~15% in 2016 to ~25% by 2022, suggesting that US investors remain selective in terms of volume but dominant in terms of capital deployed per deal.

- Both deal value and count dipped slightly after 2022, reflecting the global VC downturn, but the rebound in 2025 shows renewed US appetite, especially in AI-led investments.